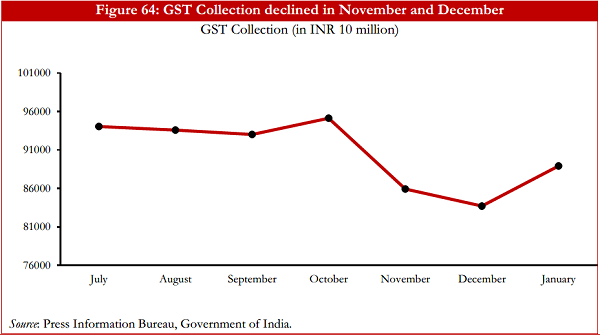

Goods and Service Tax is the most awaited legislation marked as significant indirect tax reform. It took almost 16 years when it was first suggested by the Atal Bihari Vajpayee Government in 2000 to come into existence.

World Bank in its biannual publication, The India Development Update released on March 14, 2018 state that India has the second (after Chile) highest Tax Rate i.e 28% in its four non zero tax rates i.e (5%, 12%, 18%, 28%) and also categorized as complex because of its different conditions to be satisfied to claim exemptions. According to the report it is also

admitted that introduction GST is historic move taken by the Government but as of now facing some administrative and functional issues.

Whenever any law is made the lawmaker has to consider the long term outcome of that particular law after its applicability. According to the report it is described that “the development should be considered as the start of the process and not the end”. World Bank in its press release dated March 14, 2018 also predicted the GDP Growth of India as 7.3% and

7.5% in 2018-19 and 2019-20 respectively.

Now the question is Why the report described the GST as complex?

The Indian Development Report as issued by the World Bank considered the two aspects to determine the Complexity the details rationale of which are enumerated below-

1. The number of different tax rates (including the introduction of tax exemptions)

2. The registration threshold determines which taxpayers are covered by the system.

1. The number of Different Tax Rates: The number of different tax rates (0%, 5%, 12%, 18%, 28%) determines the extent to which different products are covered. This design parameter is typically used to protect the consumption basket of the poor and achieve other social objective. With multiple tax rates imposing additional cost on compliance for business

as well as tax administration and encouraging evasion.

According to the report the extent of exemptions and sale at zero rate is a critical design parameter for GST. While exemptions allow to ease the tax burden on items with a high social value, such as healthcare, they also reduce the tax base and compromise the logic of the GST as they can: reintroduce cascading where an exempted good or service is an input into another taxable good or service; create incentives for vertical integration to keep the exempt status; and raise compliance costs by making it necessary to allocate input taxes between exempt and non-exempt output when manufactured or traded together.

2. The registration threshold: As per the report This is an instrument that government can use to relieve smaller firms from the burden of complying with GST. According to the report it is also possible to introduce a simplified system in lieu of exemptions for smaller firms which is administratively easier The disadvantage of introducing registration thresholds and

having a simplified and presumptive tax regime is that it inevitably fragments the tax system, which may reduce the tax base and provide an incentive for larger firms to mask their size and benefit from the reduced compliance burden. In addition, tax schemes that levy taxes on

sales rather than value added provide incentives for sellers to reduce their taxable sales, and potentially promoting economic inefficiencies by dis-incentivizing business growth, integration and expansion.

Conclusion: Thus the report analyse the existing GST regime from the GST Taxation system prevailing across the globe and provide a room of development which can bring the Indian GST system up to the Global standard.

(This blog is authored by Akash Goel, Secretarial Consultant)

Disclaimer: The information contained in this article is intended solely to provide general guidance on matters of interest for the personal use of the reader. Before making any decision or taking any action, the reader should always consult a professional adviser relating to the relevant article

posting.

Add Comment